The FIRE Spreadsheet That Finally Made Sense to Me

The simple 5-input FIRE spreadsheet that actually worked — from corporate burnout to early retirement in Mexico. Real numbers, honest math, no fantasy budgets.

I built my first FIRE calculator on a Tuesday night at 11:47 PM, three beers deep and absolutely furious at my job.

It was garbage. Seventeen tabs of wishful thinking and compound interest formulas that assumed I'd never buy another cup of coffee or pay for car repairs. The kind of spreadsheet that tells you you'll retire at 45 if you just live on ramen and hope.

I deleted it the next morning.

The spreadsheet that actually worked — the one that got me here, writing this from a rooftop in San Miguel de Allende — came two years later. It was simpler, meaner, and completely honest about what retirement actually costs.

The Problem With Most FIRE Calculators

Every FIRE calculator I found online made the same fatal assumption: that I'd spend less in retirement than I did while working.

Bullshit.

I wasn't planning to retire to a monk's cell. I wanted to travel, eat well, and not stress about the electric bill. The calculators that assumed I'd be happy spending $30,000 a year after decades of earning six figures were built by people who'd never actually retired.

The good ones — the brutally honest ones — were buried in Reddit threads or locked behind paywalls. So I built my own.

The Five Numbers That Matter

My final spreadsheet had exactly five inputs. Not seventeen. Five.

Current monthly spending: Not what I thought I spent. What I actually spent, averaged over twelve months of bank statements. For me, that was $8,200 in 2019. Painful to face, but necessary.

Retirement monthly spending: What I wanted to spend in retirement. I added 10% to my current spending because I planned to travel more and stress less. $9,000 per month felt honest.

Current savings: Everything. 401k, Roth IRA, taxable accounts, that savings account I forgot about. The real number: $847,000 in late 2019.

Monthly savings rate: How much I was actually putting away each month, not how much I planned to save someday. $4,200 per month, thanks to maxing out retirement accounts and living well below my tech salary.

Expected return: I used 7% because that's roughly what the S&P 500 has returned over long periods. Conservative enough to sleep at night, optimistic enough to make the math work.

The Math That Changed Everything

Here's the formula that mattered:

Annual retirement spending × 25 = Your FIRE number

That's it. The 4% withdrawal rule flipped upside down. If you need $108,000 per year ($9,000 × 12), you need $2.7 million invested.

My spreadsheet calculated how long it would take to get there:

Months to FIRE = (FIRE number - Current savings) ÷ Monthly savings ÷ Expected monthly return

The answer, in December 2019: 76 months. Six years and four months.

I was 44. I could retire at 50.

What I Got Wrong (And Right)

The spreadsheet said I'd retire in August 2026. I actually quit in March 2023.

What accelerated the timeline:

- A brutal bull market from 2020 to 2021

- Moving to Mexico, which cut my living expenses by 40% without changing my lifestyle

- Building freelance income that covered basic expenses

What the spreadsheet got exactly right:

- The psychological shift from "someday" to "specific date"

- The power of tracking real spending, not aspirational budgets

- The compound interest curve that makes the last few years of accumulation explosive

But the most important thing it got right was this: it made early retirement feel inevitable instead of impossible.

The Version That Lives on My Phone

I still have that spreadsheet. It's simpler now — just tracking our actual expenses in Mexico versus our withdrawal rate from investments.

Real numbers from October 2024:

- Monthly expenses: $2,800 (including rent, groceries, restaurants, travel)

- Monthly investment withdrawal: $3,200

- Buffer: $400 per month, which goes back into savings

The math works. More importantly, the life works.

The Spreadsheet I'd Build Today

If I were starting over, I'd add two things to those five core inputs:

Geographic arbitrage multiplier: If you're planning to move somewhere cheaper, factor it in from day one. Our move to Mexico meant we needed 40% less money than we thought. That's not luck — that's math you can plan around.

Side income goal: Even $1,000 per month in retirement income drops your FIRE number by $300,000. The peace of mind is worth even more than the math.

But I wouldn't add anything else. Complexity is the enemy of clarity. Most people never start because they're trying to model every possible scenario instead of working with the numbers in front of them.

Start With Tuesday Night at 11:47 PM

Maybe you're where I was that Tuesday night — pissed off at work and wondering if there's another way. Maybe you've built seventeen different FIRE calculators and none of them feel real.

Here's what I wish someone had told me: The perfect spreadsheet doesn't exist. The one that gets you started does.

Open Excel. Put in five numbers. See what comes out.

The worst that happens is you delete it in the morning and build a better one tomorrow. The best that happens is you realize early retirement isn't a fantasy — it's a timeline.

Some months here are leaner than others. Every month is mine.

That spreadsheet isn't just numbers anymore. It's proof.

If this resonated, The Dispatch goes deeper every week. More numbers, more stories, no spam.

More Dispatches

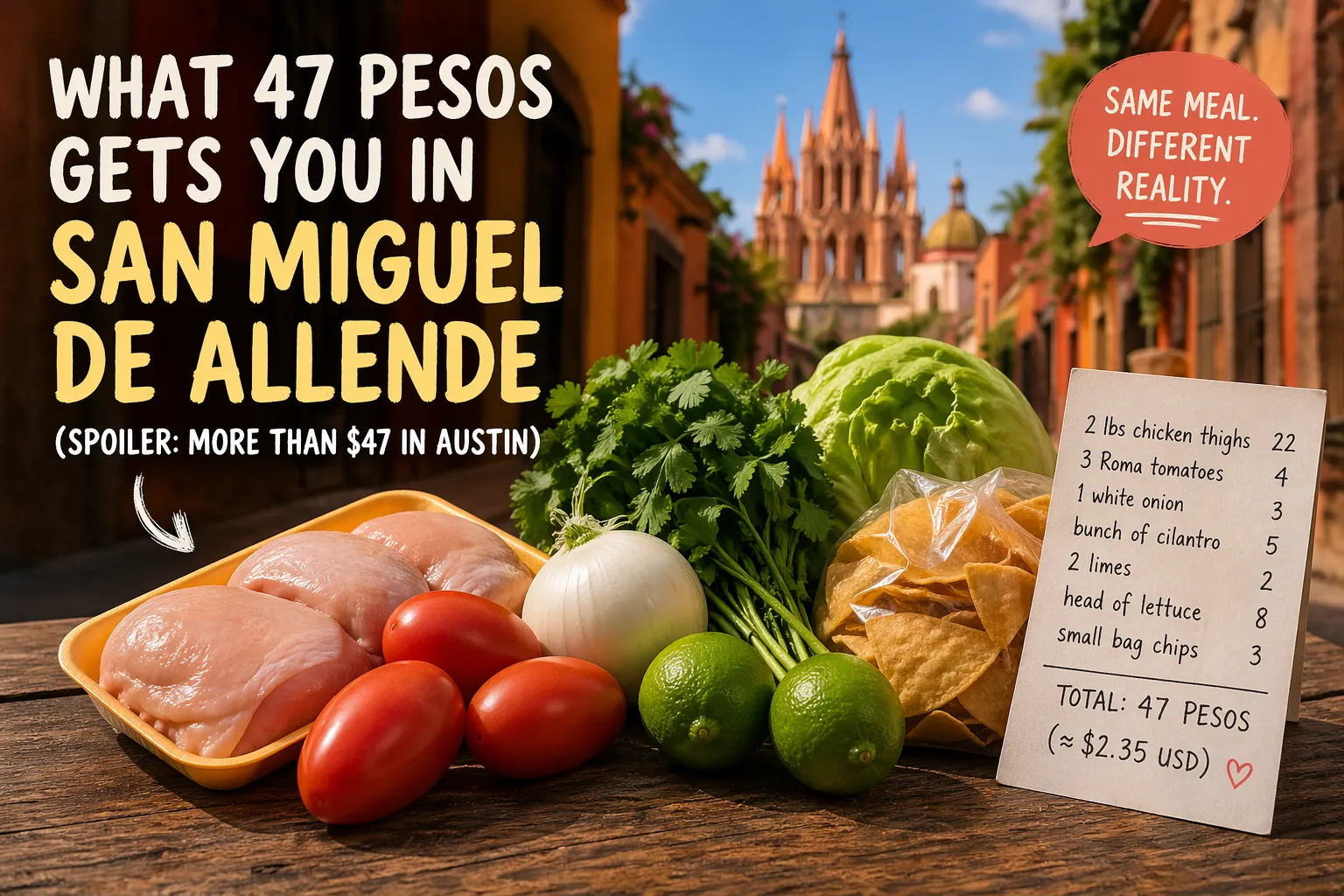

What 47 Pesos Gets You in San Miguel de Allende (Spoiler: More Than $47 in Austin)

I walked into the grocery store with 50 pesos in my pocket — about $2.50 in real money — and came out with enough food for dinner. Not ramen. Not a sad desk salad. An actual meal for three people. This is the kind of math that makes your old life feel like a fever dream. Let me break down exactly what 47 pesos bought me at the local Soriana yesterday: two pounds of chicken thighs (22 pesos), three Roma tomatoes (4 pesos), one white onion (3 pesos), a bunch of cilantro (5 pesos), two limes (2 p

Why I Ignored the 4% Rule (And Retired at 43 Anyway)

The 4% rule is gospel in early retirement circles. Pull 4% from your nest egg annually, the orthodoxy goes, and your money will last forever. Or at least thirty years, which is close enough for most spreadsheets. I ignored it completely. Not because I'm reckless with money — quite the opposite. I spent fifteen years as a corporate finance guy, building models that predicted quarterly earnings to the penny. I know how math works. I also know how life works, and life doesn't follow withdrawal ra