The Math That Changed Everything

How a simple spreadsheet at 2 AM convinced me that working until 65 was optional — and kind of insane.

It was 2 AM on a Tuesday, and I was arguing with a spreadsheet.

Not the kind of spreadsheet you'd find at work — the quarterly projections, the revenue forecasts, the endless columns of someone else's money. No. This was my money. Every dollar I'd ever earned, spent, saved, and invested, laid bare in a grid of cells that didn't care about my feelings.

I'd started the evening Googling "how to retire early" out of sheer spite. My boss had just sent an email at 11 PM asking me to "align on deliverables" for a meeting that could've been a Slack message. Somewhere between rage and resignation, I fell down a rabbit hole that would rearrange my entire life.

The Number Everyone Gets Wrong

Here's what they don't teach you in school, or at work, or at any of the financial planning seminars your company's HR department half-heartedly promotes: the age at which you can retire has almost nothing to do with your age.

Read that again.

It's not about turning 65 and collecting a gold watch. It's not about hitting some arbitrary birthday where the government says you're allowed to stop. It's about one number: your savings rate.

If you save 10% of your income, you'll work for roughly 51 years before you can retire. That's the standard playbook. Start at 22, retire at 73. Congratulations, you played yourself.

But save 50%? You're looking at about 17 years of work. Total.

Save 70%? Eight and a half years.

I stared at that calculation for a very long time.

The Spreadsheet That Broke My Brain

Here's what I plugged in that night, using numbers from my own life:

- Take-home pay: $6,200/month

- Monthly expenses: $3,800 (rent, food, car, subscriptions to things I'd forgotten I was paying for)

- Monthly savings: $2,400

- Savings rate: 39%

At that rate, assuming a 7% average return on investments, I was looking at roughly 22 years until my investment returns could cover my expenses forever. I was 31. That meant freedom at 53.

Not 65. Not 70. Fifty-three.

But then I started playing with the other side of the equation — not just earning more, but spending less. What if I ditched the car payment? Cancelled the gym I hadn't visited since February? Moved somewhere that didn't charge $2,200 a month for the privilege of hearing my neighbor's music at 1 AM?

What if my expenses weren't fixed laws of the universe, but choices I was making every single month?

I cut the spreadsheet down to $2,400/month in expenses. Aggressive, but not rice-and-beans-in-a-cave aggressive. Just... intentional. The savings rate jumped to 61%.

The new timeline: 12.5 years. Freedom at 43.

I closed the laptop. Opened it again. Checked the math. Closed it again. Poured a whiskey. Opened it one more time.

The math didn't change.

The Part Nobody Talks About

Everyone focuses on the money. The 4% rule, the index funds, the compound interest curves that look like hockey sticks. And yes, the math matters — it's the engine that makes the whole thing run.

But here's what actually changed that night: I realized I had a choice.

Not someday. Not theoretically. Right now, with the salary I already had, I could choose a fundamentally different life. Not by winning the lottery. Not by starting the next tech unicorn. Just by being deliberate about where my money went.

Every expense became a question: Is this worth an extra month of work?

That subscription box of artisanal hot sauces? One more month at the desk. The brand-new car when the used one ran fine? Eighteen more months. The apartment with the skyline view? Years.

I'm not saying you should never enjoy anything. I'm saying you should know the price — the real price, measured in your remaining years of mandatory labor.

What Happened Next

I didn't quit the next morning. I'm dramatic, but I'm not stupid.

What I did was open a brokerage account, set up automatic transfers, and start tracking every dollar with the same intensity I used to reserve for fantasy football. I renegotiated my rent. I sold the car. I cooked meals that cost $3 instead of ordering ones that cost $18.

Within six months, my savings rate hit 64%. Within a year, I'd invested more than I had in the previous five years combined.

The spreadsheet updated itself. The timeline shortened. And something else happened — something I didn't expect.

I stopped being afraid.

Not of my boss, not of losing my job, not of the economy, not of any of it. Because when you have a year of expenses in the bank and a plan that actually works, the power dynamic shifts. You're no longer working because you have to. You're working because you choose to — for now.

That's a different feeling entirely. That's the feeling of someone who knows exactly when they're walking out the door.

Your Turn

I'm not going to pretend my numbers are your numbers. Maybe you make less. Maybe you make more. Maybe you have kids, debt, a mortgage, or a sick family member. Life is complicated, and anyone who tells you early retirement is simple is selling something.

But I will tell you this: open the spreadsheet.

Plug in your real numbers. Not the ones you wish were true — the actual, uncomfortable, nobody-else-sees-these numbers. Calculate your savings rate. Run the timeline.

You might not like what you see. I didn't, at first.

But at least you'll know. And knowing — really knowing, with math instead of hope — is where everything changes.

It was for me, anyway. At 2 AM on a Tuesday, arguing with a spreadsheet that didn't care about my feelings.

If this resonated, The Dispatch goes deeper every week. More numbers, more stories, no spam.

More Dispatches

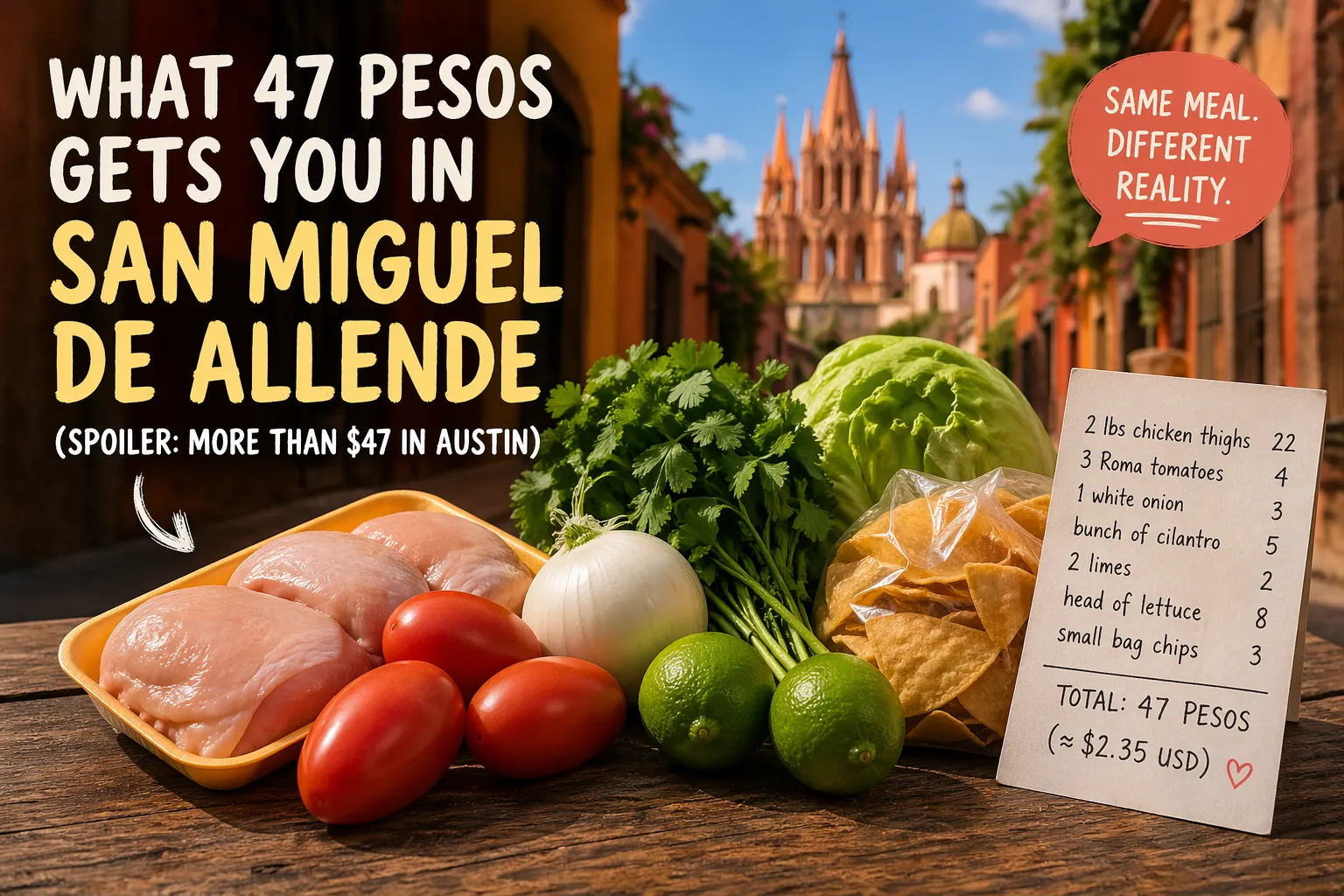

What 47 Pesos Gets You in San Miguel de Allende (Spoiler: More Than $47 in Austin)

I walked into the grocery store with 50 pesos in my pocket — about $2.50 in real money — and came out with enough food for dinner. Not ramen. Not a sad desk salad. An actual meal for three people. This is the kind of math that makes your old life feel like a fever dream. Let me break down exactly what 47 pesos bought me at the local Soriana yesterday: two pounds of chicken thighs (22 pesos), three Roma tomatoes (4 pesos), one white onion (3 pesos), a bunch of cilantro (5 pesos), two limes (2 p

Why I Ignored the 4% Rule (And Retired at 43 Anyway)

The 4% rule is gospel in early retirement circles. Pull 4% from your nest egg annually, the orthodoxy goes, and your money will last forever. Or at least thirty years, which is close enough for most spreadsheets. I ignored it completely. Not because I'm reckless with money — quite the opposite. I spent fifteen years as a corporate finance guy, building models that predicted quarterly earnings to the penny. I know how math works. I also know how life works, and life doesn't follow withdrawal ra