I retired at 42. Not because I won the lottery, not because I inherited money, and not because I discovered some secret investment hack. I ran the numbers on my own life, made some uncomfortable changes, and let compound interest do what it does.

This page is the starting point for everything I've written about the math, the strategy, and the mindset behind early retirement. If you're doing the math — or thinking about doing it — this is where you begin.

The Core Idea: Your Savings Rate Is Everything

Most people think retirement age is about age. It's not. It's about one number: the percentage of your take-home pay that you don't spend.

Here's the math that rearranged my life:

- 10% savings rate — roughly 51 working years. Start at 22, retire at 73.

- 25% savings rate — about 32 working years. Retire around 54.

- 50% savings rate — approximately 17 working years. Retire in your late 30s or early 40s.

- 70% savings rate — eight and a half years. Not a typo.

This isn't magic. It's math. Specifically, it's the relationship between how much you save, how much you need to cover your expenses, and how long your investments need to grow to produce that income perpetually. The higher your savings rate, the less you need and the faster you accumulate it. Both levers work in your favor simultaneously.

What FIRE Actually Means

FIRE — Financial Independence, Retire Early — gets a bad reputation. Some of it deserved. The internet has turned it into a performance sport where people compete to eat rice and beans for fifteen years while bragging about their spreadsheets.

That's not what this is.

Financial independence means your investments generate enough income to cover your living expenses without needing a paycheck. That's it. Whether you keep working after that point is your business. The point is that the work becomes optional.

For me, that number was roughly 25 times my annual expenses — the standard benchmark from the Trinity Study. At a 4% withdrawal rate, a portfolio of 25x your annual spending should last indefinitely, adjusted for inflation. There are arguments about whether 4% is too aggressive or too conservative. I've written about that. The short version: it's a starting point, not a religion.

How I Actually Did It

I didn't start with a plan to retire early. I started with a spreadsheet and the sinking realization that forty more years of quarterly reviews would actually kill me — maybe not literally, but close enough.

The steps were unsexy:

- I tracked every dollar for six months. Not with an app. With a spreadsheet. I needed to see exactly where money was going before I could decide what to cut.

- I cut the big things. The second car. The upgrade-every-two-years phone habit. The apartment that was 40% more expensive than it needed to be. Small optimizations matter, but the big wins are structural.

- I invested the difference aggressively. Mostly low-cost index funds. Nothing complicated. The S&P 500 doesn't care about your feelings, and over time it's beaten roughly 90% of actively managed funds.

- I ran the math every month. Not obsessively — but enough to see the trajectory. Watching the line move is the closest thing to motivation that actually works.

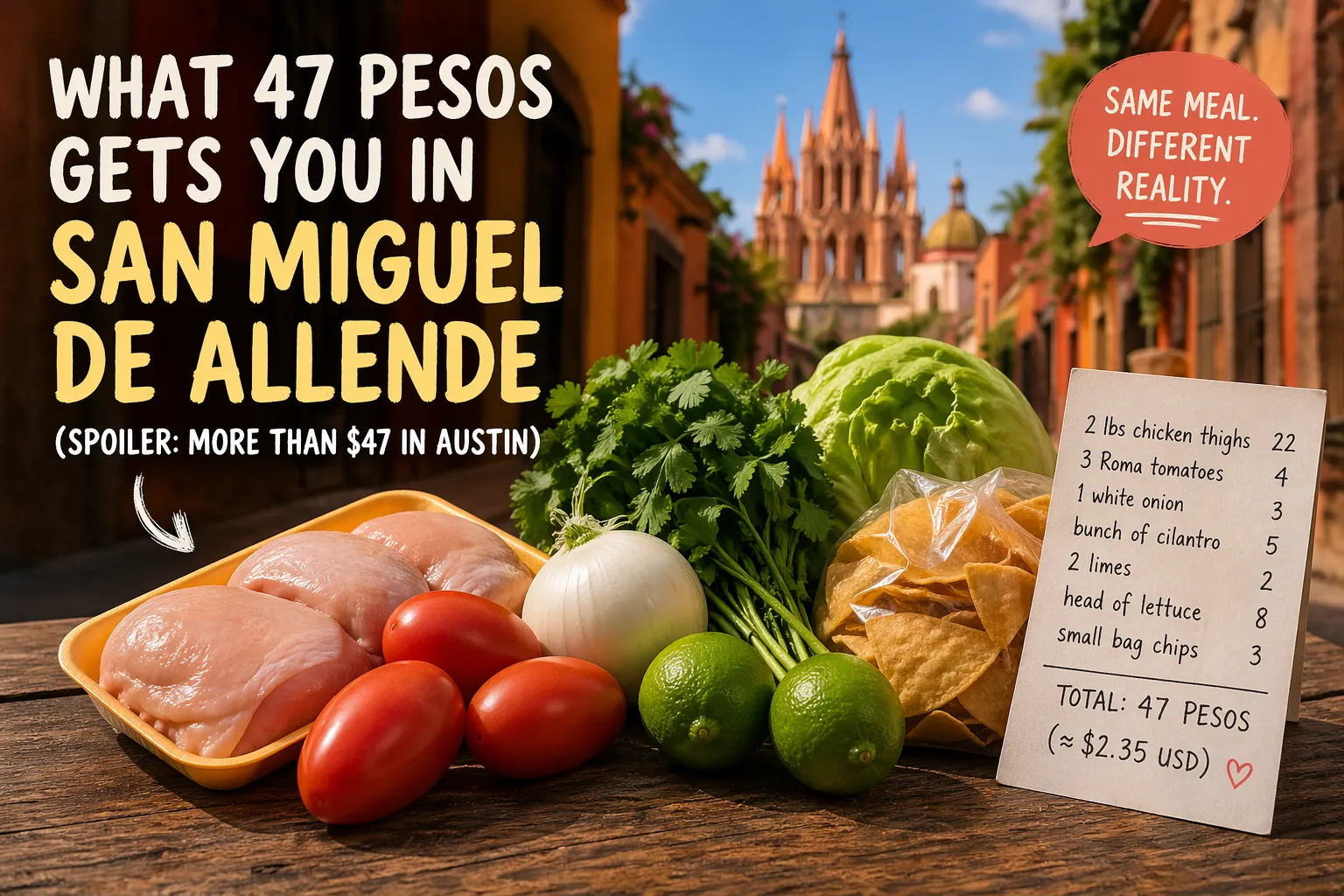

- I picked a geographic arbitrage play. Moving to Mexico wasn't just about the lifestyle. A family of three living well in San Miguel de Allende costs roughly $2,100 a month. That changes the math dramatically.

The timeline from "I should look into this" to "I'm handing in my resignation" was about eight years. I hit my number two years earlier than planned because the market cooperated and because I got more aggressive about cutting expenses as the finish line got closer.

What Nobody Tells You

The financial part is the easy part. I mean that. Once you have the math, the rest is discipline and patience — and patience is easier when you can see the countdown clock.

The hard part is everything else.

Your identity is probably tangled up in your job more than you realize. When someone at a party asks what you do, you answer with your title. When you stop having a title, that question becomes surprisingly disorienting.

Your friends will think you're crazy. Some will be genuinely worried. A few will be jealous and frame it as concern. You'll need to figure out which is which, and you'll get it wrong at least once.

The first Monday after you quit — the one where you don't have anywhere to be — is one of the strangest mornings of your life. Not bad. Strange. Like the ringing in your ears that you only notice once the noise stops.

Who This Is For

If you're a late-career professional who suspects the conventional timeline is negotiable, you're in the right place. You don't need to be in tech. You don't need a six-figure income (though it helps). You need a savings rate above 30% and the willingness to question whether the life you're living is the one you actually want.

Everything below is a dispatch from someone who did the math and followed through. Real numbers. Real timelines. Real costs — financial and otherwise.